What is Regulation Z?

Summary of Regulation Z

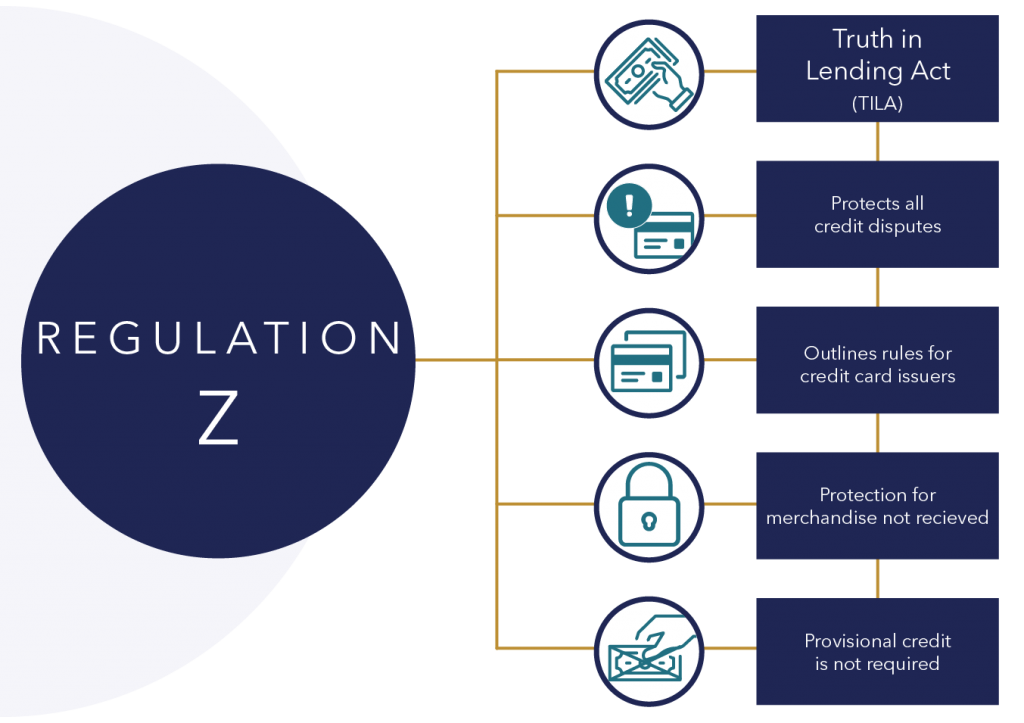

The Truth in Lending Act (TILA) of 1968 is a federal law that promotes the informed use of consumer credit. It requires standardized disclosures about the terms and cost of loans to ensure transparency in borrowing costs. Regulation Z, which implements TILA, covers various aspects of credit including credit card disclosures, periodic statements, mortgage loan disclosures, and mortgage loan servicing requirements.

Key Points and Questions

1. What is the regulation Z policy?

The regulation Z policy is a part of the Truth in Lending Act (TILA) of 1968, aimed at promoting informed use of consumer credit by requiring standardized disclosures about loan terms and costs.

2. What is an example of regulation Z?

An example of regulation Z is the prohibition of misleading terms in open-end credit advertisements. APRs cannot be referred to as fixed unless a specific time period or rate stability is mentioned.

3. What is an example of a regulation Z violation?

A common violation of regulation Z is understating finance charges for closed-end residential mortgage loans by more than the permitted $100 tolerance.

4. What does regulation Z apply to?

Regulation Z applies to credit card disclosures, periodic statements, mortgage loan disclosures, and mortgage loan servicing requirements.

5. What is the Dodd Frank regulation Z?

The Dodd-Frank Wall Street Reform and Consumer Protection Act amended TILA by requiring the annual adjustment of the dollar threshold for exempt consumer credit transactions.

6. Who enforces regulation Z?

The Federal Trade Commission (FTC) enforces regulation Z with regard to most non-bank entities.

7. Who does regulation Z apply to?

Regulation Z applies to consumers and protects them from misleading practices by the credit industry. It applies to various types of loans including home mortgages, home equity lines of credit, reverse mortgages, credit cards, installment loans, and certain student loans.

8. What loans are exempt from regulation Z?

Loans with a business or agricultural purpose, and certain student loans are exempt from regulation Z. Credit for acquiring or improving rental property that is not owner-occupied is also considered business purpose credit.

9. What does regulation Z not cover?

Regulation Z does not apply to rules of issuance and unauthorized use liability for credit cards. It also does not cover loans with a business or agricultural purpose, and certain student loans.

10. What is the difference between Reg E and Reg Z?

Regulation E protects consumers from predatory lending practices and standardizes the sharing of borrowing costs, while regulation Z is relevant for specific types of credit including credit cards, mortgages, home equity lines of credit, installment loans, and some student loans.

11. Why is regulation Z important?

Regulation Z is important because it ensures lenders provide borrowers with written access to interest rates, fees, and finance charges. It also requires lenders to provide monthly billing statements to borrowers.

What is the regulation Z policy

The Truth in Lending Act (TILA) of 1968 is a Federal law designed to promote the informed use of consumer credit. It requires disclosures about the terms and cost of loans to standardize how borrowing costs are calculated and disclosed.

CachedSimilar

What is an example of regulation Z

Regulation Z prohibits misleading terms in open-end credit advertisements. For example, an advertisement may not refer to APRs as fixed unless the advertisement also specifies a time period in which the rate will not change or that the rate will not increase while the plan is open.

What is an example of a regulation Z violation

Common Violations

A common Regulation Z violation is understating finance charges for closed-end residential mortgage loans by more than the $100 tolerance permitted under Section 18(d).

What does the regulation Z apply to

The regulation covers topics such as:

Credit card disclosures. Periodic statements. Mortgage loan disclosures. Mortgage loan servicing requirements.

Cached

What is the Dodd Frank regulation Z

The Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank Act) amended TILA by requiring that the dollar threshold for exempt consumer credit transactions be adjusted annually by the annual percentage increase in the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W).

Who enforces regulation Z

Regulation Z (TILA)

The FTC enforces TILA and its implementing Regulation Z with regard to most non- bank entities.

Who does regulation Z apply to

Regulation Z protects consumers from misleading practices by the credit industry and provides them with reliable information about the costs of credit. It applies to home mortgages, home equity lines of credit, reverse mortgages, credit cards, installment loans, and certain kinds of student loans.

What loans are exempt from regulation Z

Coverage Considerations under Regulation Z

(Exempt credit includes loans with a business or agricultural purpose, and certain student loans. Credit extended to acquire or improve rental property that is not owner-occupied is considered business purpose credit.)

What does regulation Z not cover

Coverage Considerations under Regulation Z

Regulation Z does not apply, except for the rules of issuance of and unauthorized use liability for credit cards. (Exempt credit includes loans with a business or agricultural purpose, and certain student loans.

What is the difference between Reg E and Reg Z

Regulation E vs.

It protects consumers from predatory lending practices and standardizes how lenders must share the cost of borrowing with consumers. As mentioned, Regulation Z is relevant for credit cards, mortgages, home equity lines of credit, installment loans, and some student loans.

Why is regulation Z so important to us

Under the regulation, lenders are required to provide borrowers with access to interest rates, fees and finance charges in writing. Other aspects of the law include: Lenders must provide monthly billing statements to borrowers.

What is the penalty for regulation Z

The Consumer Financial Protection Bureau (Bureau) proposes to amend Regulation Z, which implements the Truth in Lending Act (TILA), to better ensure that the late fees charged on credit card accounts are “reasonable and proportional” to the late payment as required under TILA.

What loans are not covered by Reg Z

The following loans aren't subject to Regulation Z laws: Federal student loans. Credit for business, commercial, agricultural or organizational use. Loans that are above a threshold amount.

What type of loan is covered by regulation Z

Key Takeaways. Regulation Z protects consumers from misleading practices by the credit industry and provides them with reliable information about the costs of credit. It applies to home mortgages, home equity lines of credit, reverse mortgages, credit cards, installment loans, and certain kinds of student loans.

What is Regulation Z ability to repay and qualified mortgage rules

Regulation Z generally prohibits a creditor from making a mortgage loan unless the creditor determines that the consumer will have the ability to repay the loan.

What is the difference between Regulation Z and respa

The Truth in Lending Act and Regulation Z are almost identical. TILA is a law, while Regulation Z is a Federal Reserve regulation. They both require full disclosure of the costs and terms associated with credit financing. RESPA is a law which requires full disclosure of settlement costs.

Who does Regulation Z apply to

Regulation Z or TILA applies to mortgages, home equity loans, HELOCs, credit cards, installment loans and private student loans. The act does not govern actual loan terms, dictate who can apply for credit, or direct lenders to offer certain types of loans.

Is Reg Z the same as TILA

The TILA amendments of 1995 dealt primarily with tolerances for real estate secured credit. Regulation Z was amended on September 14, 1996 to incorporate changes to the TILA. Specifically, the revisions limit lenders' liability for disclosure errors in real estate secured loans consummated after September 30, 1995.

What is the difference between regulation Z and TILA

The TILA amendments of 1995 dealt primarily with tolerances for real estate secured credit. Regulation Z was amended on September 14, 1996 to incorporate changes to the TILA. Specifically, the revisions limit lenders' liability for disclosure errors in real estate secured loans consummated after September 30, 1995.

What violates regulation Z in real estate

Regulation Z prohibits practices in which mortgage brokers and loan originators may receive compensation for referrals or "steering." So, say that you want to buy a home. You connect with a real estate agent, who then refers you to a specific mortgage lender. The agent receives no compensation for this referral.

Does Regulation Z apply to all loans

Regulation Z or TILA applies to mortgages, home equity loans, HELOCs, credit cards, installment loans and private student loans. The act does not govern actual loan terms, dictate who can apply for credit, or direct lenders to offer certain types of loans.

What kinds of loans are eligible for a three day right of rescission under regulation Z

Established by the Truth in Lending Act (TILA) under U.S. federal law, the right of rescission allows a borrower to cancel a home equity loan, home equity line of credit (HELOC), or refinance with a new lender, other than with the current mortgagee, within three days of closing.

What is a Reg Z qualified mortgage

With certain exceptions, Regulation Z requires creditors to make a reasonable, good faith determination of a consumer's ability to repay any residential mortgage loan, and loans that meet Regulation Z's requirements for “qualified mortgages” (QMs) obtain certain protections from liability.

What is the ability to repay Regulation Z criteria

Regulation Z generally prohibits a creditor from making a mortgage loan unless the creditor determines that the consumer will have the ability to repay the loan.

What is the difference between Regulation Z and TILA

The TILA amendments of 1995 dealt primarily with tolerances for real estate secured credit. Regulation Z was amended on September 14, 1996 to incorporate changes to the TILA. Specifically, the revisions limit lenders' liability for disclosure errors in real estate secured loans consummated after September 30, 1995.